Forecasting: Science and Art

There are few skills associated with managing staff that have bigger potential benefits or pitfalls than forecasting. Get it right and staff morale will improve, customer service will be better and the budget is more likely to be on target. Get it wrong and staff may be overworked or bored, customer service may be great or terrible, and the budget will not be based on reality. If no attempt is made to forecast at all the results could be any of the above, but more from luck than management.

A simple definition of forecasting is predicting a specific requirement for some point in the future. It matters less what is being forecasted (stock prices, branches, staff, inventory, etc.), but rather how the forecast is created and its accuracy. This article focuses on forecasting staff for bank and credit union branches and call centers.

Data, Data, Data

At the core of any forecast is data, and more is better. Without data the exercise is a guess, not a forecast. There are, of course, many kinds of data and many ways to gather it. Two data sources commonly used in forecasting for banks and credit unions are transaction timings and transaction data.

Transaction timing studies seem an obvious choice and many clients ask about them. Done properly, a timing study can provide valuable initial information. Some studies are done with observers in live customer environments while others are conducted in a controlled lab environment. The key is to make sure the sample is large enough, diverse enough, and represents a realistic mix of transactions and market conditions. Regardless of how the study is done, a weakness of timing studies is that they represent a snapshot in time of a limited sample of transactions. A rigorous timing study is also a significant investment in planning, effort and cost. Consequently, few institutions conduct timing studies more than once, so that forecasts are based on increasingly obsolete information.

Virtually all commercial software that provides forecasting and scheduling is going to capture transaction data in some way. Not all systems use that data to generate the forecast, but rather for reporting or validating the forecast. Generating the forecast from transaction data means performing periodic statistical analysis on the data. The key to generating forecasts from transaction data is to continuously gather as much information as possible.

- Capture as many types of transaction information as possible: teller transactions, inquiries, account maintenance, account openings, etc.

- Where available collect associated activities such as image capture, ATM or cash automation maintenance, cash ordering, inventories, etc.

- Factor in the mix of transactions, preferably weighted to reflect the volume and overhead.

- Include cash handling and volume for teller data.

- For Call Centers raw call data is best, but if using aggregated data then 15 minute or a maximum of 30 minute time blocks should be used.

- Anything else that can be captured which represents overhead to the operation.

The more different data sources that can be fed into the forecasting model, the more complete a picture the forecast can be based on.

Developing A Forecast

Many different methodologies can be used to generate a good, or poor, forecast. There is not an accepted standard methodology, there is no one "right" answer, and it is possible to use anything from sophisticated commercial software applications to spreadsheets.

The most important aspect of any forecast is that it be valid for the specific operational environment and market it is being applied to. A branch where every teller is supported by a cash recycler is not the same operational environment as a branch with no cash automation. A branch in downtown Manhattan does not work the same as a branch in Fairfield Iowa. A branch with a high percentage of commercial customers should not be forecast the same way as a branch that is exclusively consumer.

That means regardless of what tools and methodologies are used, the process of creating a forecast must be adaptable to the environment it is forecasting. Variability exists between institutions and geographic regions, but may also exist within a single institution. Call centers have different characteristics and need shorter forecast timeframes than branches, so forecasting methods need to accommodate the differences.

Prospective clients routinely ask what the standard or average or normal amount of staff is. That question leads to misleading answers. A better question is what the optimum level of staff is for your institution given your operation, market and culture.

One contribution to developing a forecast that is often overlooked, is institutional knowledge and experience. While statistical analysis may form the nucleus of a forecast, it should be complemented and validated by institutional knowledge. People who have been managing branches and branch staff have a good sense of what works. Put it to use.

Using Forecasts

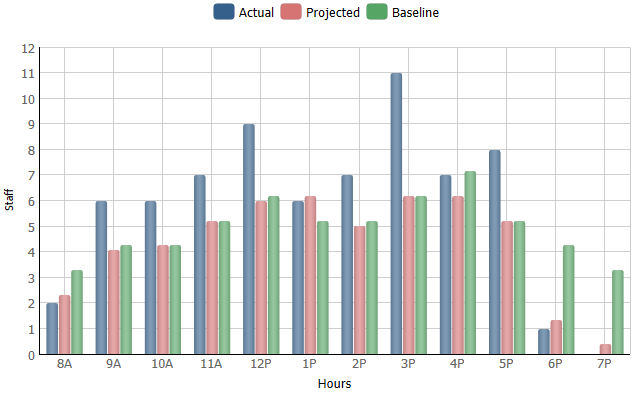

Depending on the systems available there are many ways to utilize a forecast. Forecasting and scheduling software will automatically use the forecast to help create schedules. These systems will generally also report or display how the forecast compares with actual branch schedules. Institutions without formal scheduling software should effectively do the same thing. Look at the forecast to help determine what the schedule should be, and periodically review how well actual schedules match the forecast.

The key is for the forecasts to be easily accessible to the personnel creating and evaluating the schedules. Forecasts work best when they are part of the operation on an ongoing basis. If an institution goes to the trouble of developing a forecast but only one person in management has it, the forecast is of limited value. Having software specifically designed to do this makes it easier, but the need and benefit are the same regardless.

Forecasts can be an effective form of feedback for both branch personnel and management. Particularly when forecasts are based on recent data and refreshed regularly, branches can see that they are still on track and get early detection of when needs are evolving away from schedules. Comparison to budget is useful feedback, but is looking backward. An up-to-date forecast is predictive. Management gets an objective tool for evaluating branch schedules during the year, and gains a powerful tool to help develop next year's budget.

No matter how accurate or recent a forecast is, it cannot measure everything. By definition forecasts are an extrapolation of a set of events that have already occurred. Therefore, it is important to maintain a perspective that while forecasts are an important reference, they are not an edict or a weapon. Real life will always vary from a forecast, it is only a question of by how much.

A forecast, and/or the data that supports it, is an excellent source of information for evaluating branch hours, particularly extended or weekend hours. Multiple clients have told us that they have modified branch hours based on the forecasts and utilization information provided by the system. Variability of hours within a branch network is now common, customers are not surprised by it, and online tools make it easy for them to find the nearest open branch. Forecasts help make these decisions be objective.

Investing in the ability to forecast can and should be a good business decision in addition to benefitting the operation. Even comprehensive commercial software designed for forecasting and scheduling generally costs about the same as one average FTE for every 20 locations. In house solutions may cost less up front, but make sure that they are fully automated, so ongoing overhead does not build up. The exercise to develop a good forecast, keeping it updated, then putting it to use all have concrete benefits for banks and credit unions.